Term Insurance For Salaried Professionals

A regular salary often supports more than monthly expenses. From home loans and family responsibilities to long-term goals, financial commitments usually continue regardless of circumstances.

Term insurance helps create financial protection around the people and responsibilities that depend on your income.

Why Salaried Professionals Consider Term Insurance

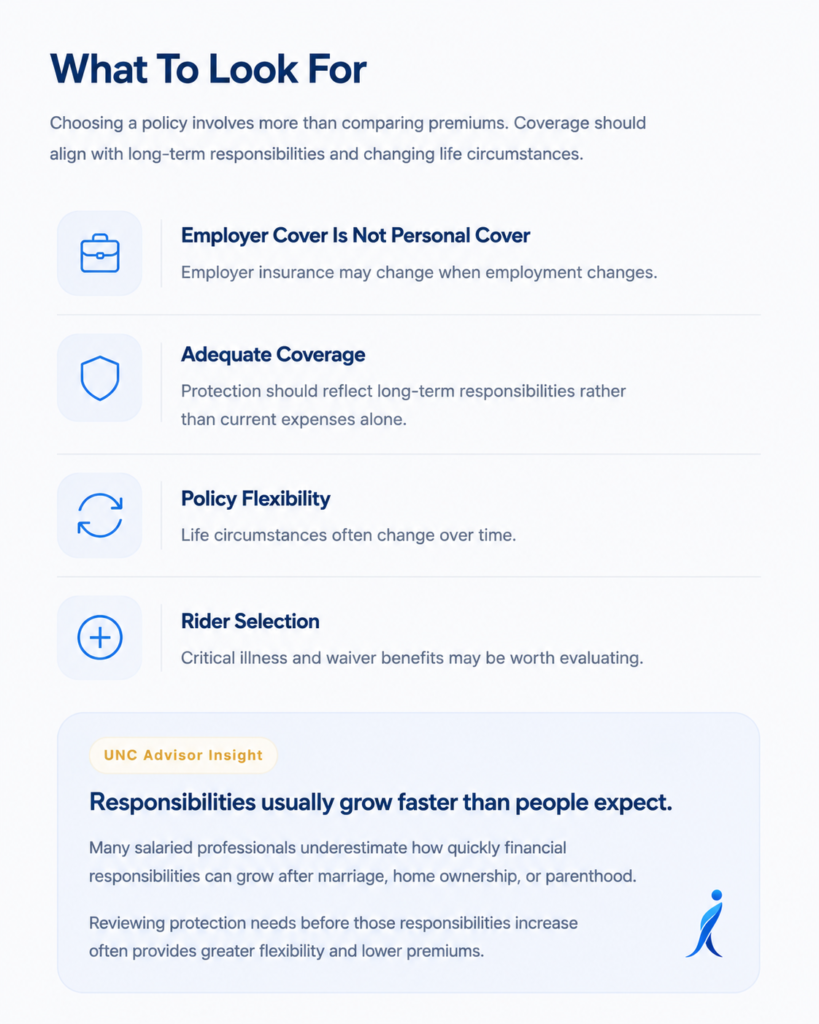

Many working professionals rely on employer-provided life insurance without realising it may not be enough to support long-term family needs.

Common responsibilities include:

✓ Home Loans

✓ Family Expenses

✓ Children’s Education

✓ Dependent Parents

✓ Future Financial Goals

UNC Recommended Plans

Plans Commonly Considered By Salaried Professionals

Cover Continuance Benefit

Waiver Of Premium Options

Critical Illness Rider

Flexible payout options

Policy flexibility

Flexible benefit structures

Affordable premium structure

Insurance made simple. Expert advice, tailored to your needs.

Book a free consultation or chat on WhatsApp with a UNC Insurance advisor.

Typical Premium Range

For a healthy non-smoking salaried professional aged 30

₹2 Crore cover till age 70 may typically start from:

Speak With a Human Advisor

✓ Rated 5.0/5 on Google Reviews

✓ Clear Guidance Without Pressure

✓ Dedicated Claim Assistance

✓ Support Before and After Policy Purchase

✓ Personalized Recommendations Based on Your Needs

✓ 100% Free Consultation

Have questions? Book a callback or chat with an advisor on WhatsApp. We’re here whenever you need assistance.

Frequently

Asked

Questions

Customer Reviews

I had a very smooth experience. Everything was explained clearly and patiently, which made it much easier to understand my options. I appreciated the transparency and the fact that there was never any pressure during the process.

What stood out the most was the responsiveness and professionalism. Every question was answered in a simple manner, and the entire experience felt trustworthy from start to finish.

I was looking for guidance rather than a sales pitch, and that is exactly what I received. The explanations were easy to understand and helped me make a more informed decision.

Great service and clear communication. Everything was explained in a practical way, and I always felt supported whenever I needed assistance.