Parents’ Coverage

Health insurance for parents often requires a different approach than health insurance for younger individuals or families. As people age, healthcare needs, medical consultations, diagnostic tests, hospitalization requirements, and the likelihood of claims may increase, making adequate coverage an important consideration.

Many families initially focus on their own health insurance needs and postpone planning for their parents’ healthcare protection. However, rising medical costs, increasing life expectancy, and the growing prevalence of age-related health conditions have made dedicated health insurance for parents an essential part of comprehensive financial planning.

When evaluating health insurance plans for parents, factors such as age, existing medical conditions, waiting periods, coverage benefits, network hospitals, claim support, and sum insured become particularly important. A policy that works well for a younger family may not always be the most suitable option for senior members.

Key Considerations for Parents’ Health Insurance before choosing a health insurance plan for parents, it is helpful to assess:

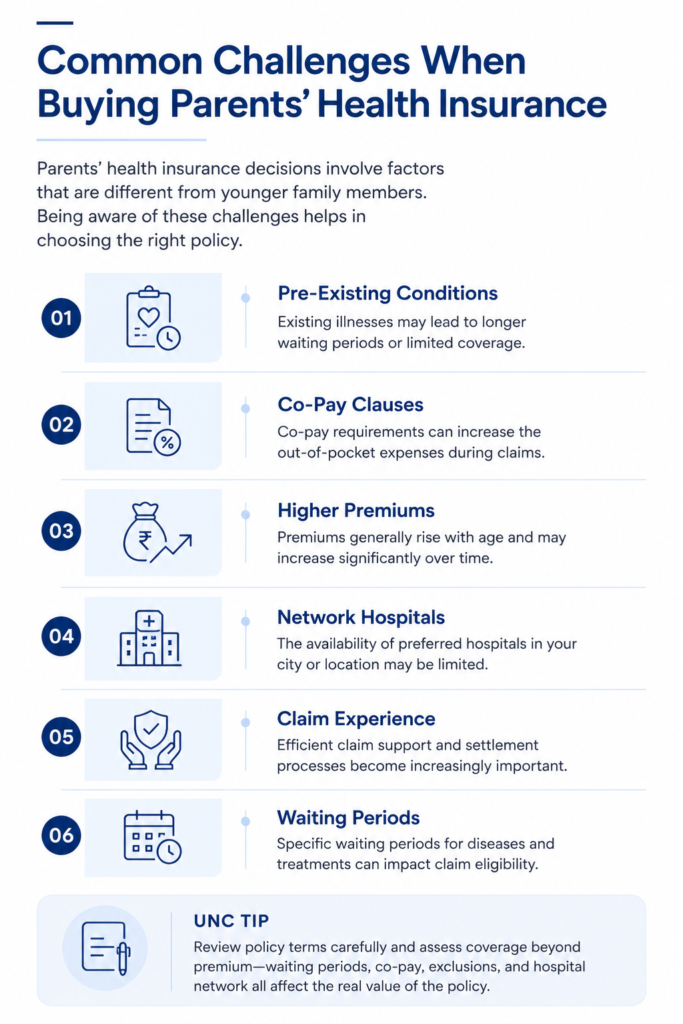

1.Age and current health status

2.Pre-existing medical conditions

3.Waiting period requirements

4.Hospitalization and treatment coverage

5.Sum insured adequacy

6.Network hospital availability

7.Long-term affordability and renewal options

At UNC Insurance, we help families across Delhi, Delhi NCR, Gurugram, Noida, Faridabad, and Ghaziabad understand the factors involved in selecting health insurance for parents. Our advisory approach focuses on comparing coverage options, evaluating policy features, and helping families make informed decisions that align with their healthcare and financial goals.

UNC Recommended Plans

Plans Commonly Considered For Parents’ Health Coverage

Wellness Ecosystem

Restoration Benefits

Long-Term Flexibility

Strong Restoration Features

Long-Term Coverage Flexibility

Essential Health Coverage

Balanced Protection Features

Typical Premium Range

Parents (60–65 Years)

Insurance made simple. Expert advice, tailored to your needs.

Book a free consultation or chat on WhatsApp with a UNC Insurance advisor.

Speak With a Human Advisor

✓ Rated 5.0/5 on Google Reviews

✓ Clear Guidance Without Pressure

✓ Dedicated Claim Assistance

✓ Support Before and After Policy Purchase

✓ Personalized Recommendations Based on Your Needs

✓ 100% Free Consultation

Have questions? Book a callback or chat with an advisor on WhatsApp. We’re here whenever you need assistance.

What Matters Most

Premiums are important, but they are rarely the only factor that influences the long-term suitability of parents’ health insurance coverage.

PED Waiting Period

Pre-existing disease waiting periods can significantly affect when coverage becomes available for existing medical conditions.

Co-Pay Clauses

Some plans require policyholders to share a percentage of claim costs, increasing out-of-pocket expenses.

Network Hospitals

A strong cashless hospital network can make treatment access easier and reduce claim-related stress.

Claim Experience

Service quality, claim responsiveness, and policy support often become increasingly important as healthcare usage grows.

Frequently

Asked

Questions

Customer Reviews

I had a very smooth experience. Everything was explained clearly and patiently, which made it much easier to understand my options. I appreciated the transparency and the fact that there was never any pressure during the process.

What stood out the most was the responsiveness and professionalism. Every question was answered in a simple manner, and the entire experience felt trustworthy from start to finish.

I was looking for guidance rather than a sales pitch, and that is exactly what I received. The explanations were easy to understand and helped me make a more informed decision.

Great service and clear communication. Everything was explained in a practical way, and I always felt supported whenever I needed assistance.