How Much Life Insurance Cover Is Enough?

One of the most common misconceptions about health insurance is that it can wait until later in life. In reality, the best time to purchase health insurance is often before you need it.

For young professionals, health insurance is not just about protecting against unexpected medical expenses—it’s about building long-term financial security. Starting early can help you secure coverage while you’re younger, healthier, and typically less likely to face restrictions related to pre-existing medical conditions.

As careers grow and responsibilities increase, healthcare needs can change quickly. Whether you’re working in Delhi, Gurugram, Noida, Faridabad, Ghaziabad, or elsewhere in Delhi NCR, a medical emergency, hospitalization, or unexpected illness can create significant financial pressure without adequate health insurance coverage.

Why Early Planning Matters

Purchasing health insurance early can offer several advantages:

1.Protection against unexpected hospitalization expenses

2.Access to health coverage before major medical needs arise

3.Earlier completion of policy waiting periods

4.Long-term continuity of coverage

5.Reduced reliance on employer-provided health insurance alone

6.Better preparation for future healthcare costs

At UNC Insurance, we help young professionals across Delhi and Delhi NCR understand health insurance options, compare coverage features, and choose plans that align with their current needs and future goals. The right policy today can help create stronger healthcare and financial protection for the years ahead.

UNC Recommended Plans

Plans Commonly Considered By Young Professionals

Wellness Rewards

Long-Term Policy Continuity

Flexible Coverage Options

Strong Bonus Structure

Coverage Growth Features

Essential Health Coverage

Cost-Effective Protection

Typical Premium Range

Individual · Age 25–30

Insurance made simple. Expert advice, tailored to your needs.

Book a free consultation or chat on WhatsApp with a UNC Insurance advisor.

Speak With a Human Advisor

✓ Rated 5.0/5 on Google Reviews

✓ Clear Guidance Without Pressure

✓ Dedicated Claim Assistance

✓ Support Before and After Policy Purchase

✓ Personalized Recommendations Based on Your Needs

✓ 100% Free Consultation

Have questions? Book a callback or chat with an advisor on WhatsApp. We’re here whenever you need assistance.

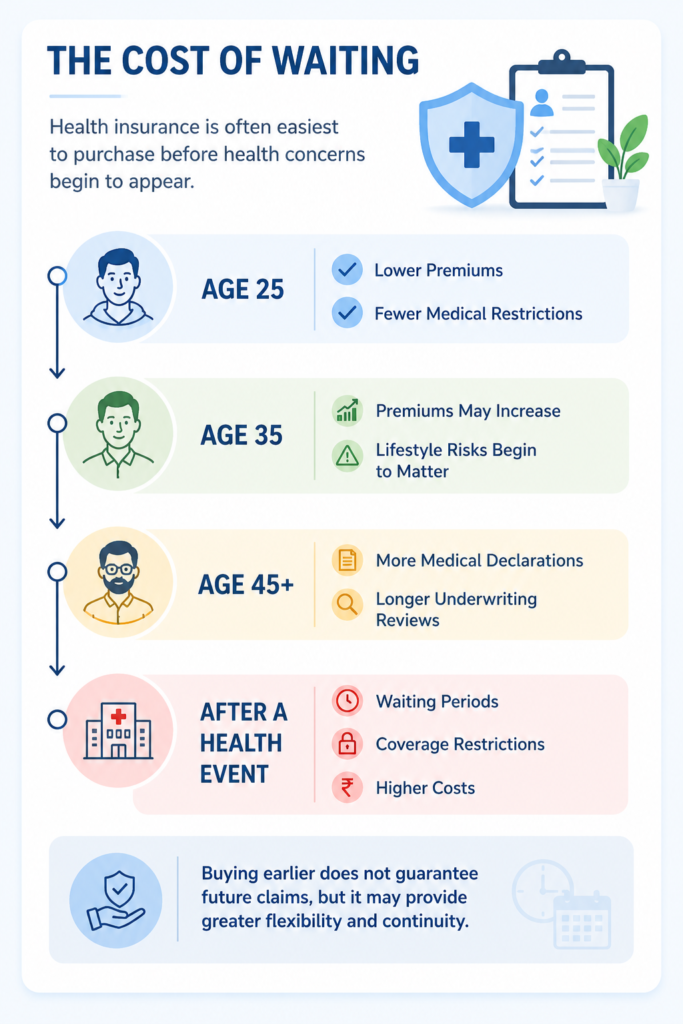

Why Buy Early?

Health insurance is often easiest to obtain before significant healthcare needs arise. Early coverage can provide long-term advantages beyond premium savings alone.

Lower Premiums

Premiums are generally lower at younger ages, making long-term coverage more affordable.

Fewer Medical Restrictions

Purchasing coverage earlier may reduce the impact of future medical disclosures and underwriting requirements.

Waiting Period Completion

Waiting periods can often be completed while you remain healthy and may not need immediate treatment.

Long-Term Continuity

Maintaining continuous coverage can simplify future healthcare planning as life circumstances evolve.

UNC Advisor Insight

Many people buy health insurance after a medical concern arises. By then, underwriting and waiting periods become more important.

Frequently

Asked

Questions

Customer Reviews

I had a very smooth experience. Everything was explained clearly and patiently, which made it much easier to understand my options. I appreciated the transparency and the fact that there was never any pressure during the process.

What stood out the most was the responsiveness and professionalism. Every question was answered in a simple manner, and the entire experience felt trustworthy from start to finish.

I was looking for guidance rather than a sales pitch, and that is exactly what I received. The explanations were easy to understand and helped me make a more informed decision.

Great service and clear communication. Everything was explained in a practical way, and I always felt supported whenever I needed assistance.